The Sketchbook of Wisdom:Â A Hand-Crafted Manual on the Pursuit of Wealth and Good Life

Buy your reprinting of the typesetting Morgan Housel calls “a masterpiece.” It contains 50 timeless ideas – from Lord Krishna to Charlie Munger, Socrates to Warren Buffett, and Steve Jobs to Naval Ravikant – as they wield to our lives today. Click here to buy now.

In the endnotes of his sunny book, Winning the Loser’s Game, Charles Ellis wrote well-nigh two of his weightier friends who, at the peak of their distinguished careers in medicine, well-set that the two most important discoveries in medical history were penicillin and washing hands (which stopped the spreading of infection from one mother to flipside via the midwives who delivered most babies surpassing 1900).

Ellis’s friends moreover counselled him there was no largest translating on how to live longer than to quit smoking and to buckle up when driving.

The lesson Ellis leaves the reader with is this –

“Advice doesn’t have to be complicated to be good.”

I have been an investor for 20 years, which has been a good unbearable time to make me enlightened of a profound investor bias toward complexity.

Over these years, I have seen too many investors trying to fight complexity by subtracting plane increasingly complexity into their investment process and financial lives.

The world, you know, is complex. And so are financial markets.

Amidst this, how do you deal with such complexity in your wealth megacosm journey without losing your sanity?

I believe the wordplay is to have a personal financial plan that is elegant in its simplicity.

And so, when it comes to my own money and finances, I try to alimony it very simple.

Like this simple financial plan that I have been practicing for the past few years, and one that has served me very well.

Personal finance is, well, personal. But I hope this outline helps you in reviewing your own finances to find out the

So, here’s my simple personal financial plan –

- Earn increasingly money than I need now (amidst too much focus on saving money, working nonflexible to earn increasingly is an underrated idea. But I believe it holds unconfined importance. I can only save so much. But I can work nonflexible to earn much more.)

- Save money (first save, then spend)

- Emergency fund (around 8-12 months of household expense, saved in a wall worth or liquid fund)

- Medical and life/term insurance (I do not need any other forms of insurance)

- Invest the rest – (a) Money needed in <5 years – Allocate increasingly to debt (this is money I would need in the short term, and so I focus increasingly on wanted protection here than any return), and (b) Money needed in >5 years – Allocate increasingly to probity (this is money I would need in the long term, and so I focus increasingly on wanted appreciation that’s faster than rate of inflation. Also, I stave investments that can destroy this money permanently)

- Write a Will (I understood the importance late, but now working towards it)

- Avoid debt (all upper forfeit debt, like credit vellum debt, personal loans, etc.)

- Document (so important to let myself and my family know what I am up to)

- Review every 6 months (maybe, 12 months. Not to tinker around, but just to trammels if things are moving in the right direction).

Oliver Wendell Holmes, the American physician, poet, and humorist, said –

I wouldn’t requite a fig for the simplicity on this side of complexity, but would requite my life for the simplicity on the other side of complexity.

Simple can be harder than complex. You have to work nonflexible to get your thinking wipe to make it simple. But then, as Steve Jobs said in an interview in 1988 –

…it’s worth it in the end considering once you get there, you can move mountains.

That’s moreover true for managing your personal finances. In practicing simplicity, and staying the course, over time you can moreover move mountains.

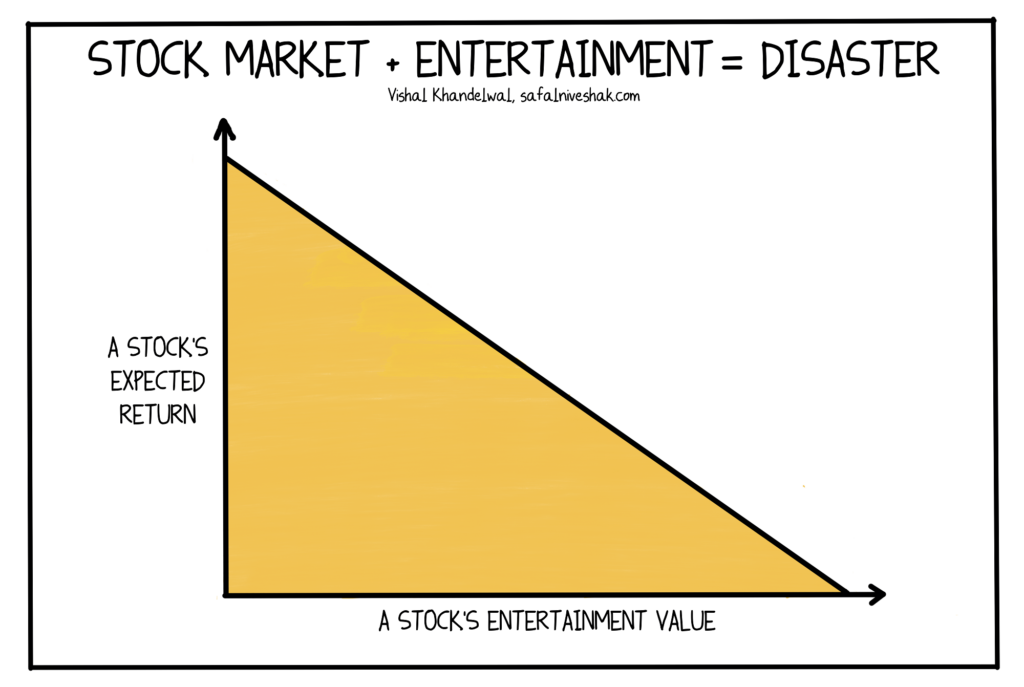

Stock Market Entertainment = Disaster

Paul Samuelson wrote –

Investing should be increasingly like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.

There is no denying that a lot of investors like to have “good looking” portfolios, invested in the period’s most heady industries.

For them, my translating is to resist the temptation.

An investment’s long term expected return correlates inversely with its short term entertainment value.

Greater the entertainment now (hot stocks, IPOs), lower the long term expected return.

Lower the entertainment now (boring businesses), greater the long term expected return.

So, segregate your investments well. Seek what is good for your in the long run, not what makes you ‘feel’ good in the short run.

Reasons to Stay Alive

One of the weightier short books I have read in recent times is Matt Haig’s Reasons to Stay Alive.

A passage from the typesetting reads –

And most of all, books. They were, in and of themselves, reasons to stay alive. Every typesetting written is the product of a human mind in a particular state. Add all the books together and you get the end sum of humanity. Every time I read a unconfined typesetting I felt I was reading a kind of map, a treasure map, and the treasure I was stuff directed to was in very fact myself.

If you are feeling down, or anxious, or panic stricken, or depressed, or just seeking an inspirational boost, this typesetting will pick you up. Read it.

That’s well-nigh it from me for today.

Thank you for your time.

If you are seeing this newsletter for the first time, you may subscribe here.

Regards,

Vishal

The post My Personal Financial Plan appeared first on Safal Niveshak.