Investing for the long term is the key to financial security, but the greatest investments alter over time, depending on how the market and economy perform.

I’ve narrowed down the ten finest investments right now to help you get your assets on track to reach your objectives.

1. High-Yield Savings Accounts

High-yield savings accounts may not feel like an investment, but they offer compound earnings and little to no risk, so they are a fantastic option for a conservative and liquid investment.

HYSAs pay high-interest rates because most institutions that offer them have little to no overhead because they operate online and do not have a brick-and-mortar location.

The good part about HYSAs is you aren’t investing. You automatically know the interest rate you’ll earn; if you leave the interest, it will compound further. HYSAs are excellent for investors who need a liquid investment they can access when required.

They are also a diversification instrument to mitigate the risk of more aggressive investments, as there is no relation to the stock market.

Pros

-

Pays much higher interest rates than local institutions, and they typically don’t have monthly fees or minimum balance requirements.

-

Interest often compounds daily, allowing your savings to grow speedier

-

You can access your administer your accounts 24/7

Cons

-

Interest rates can fluctuate; there’s no way to foretell how they’ll perform

-

Inflation can outpace interest rates, making it challenging to reach long-term objectives

-

Your withdrawals are limited to six per month

2. Short-Term Certificates of Deposit

Short-term certificates of deposit are often a superior method to invest money than a savings account. Still, because C.D.s necessitate an investment for a specific duration, short-term C.D.s are ideal, particularly when interest rates are higher.

C.D.s are an excellent short-term investment for anyone seeking to add a prudent investment to their portfolio or increase the capital they don’t need immediately. Short-term CDs are often preferable than long-term because they offer flexibility to reinvest the funds in something with a higher rate during periods of inflation.

Understanding the term and only investing in CDs you can leave undisturbed is essential. If you withdraw funds early, you will pay a penalty, usually equal to three months of interest.

Pros

-

Often yields a larger interest rate than savings accounts

-

It offers a low-risk investment, particularly if you invest funds in an FDIC-insured bank

-

Have a fixed term so you know when you’ll get your principal back

Cons

-

Your money is sealed up for the entire term (or there is a fee)

-

The interest collected is taxable

-

CD rates don’t often keep up with inflation, so the shorter the tenure, the better

3. S&P 500 Index Funds

The S&P 500 index is the most monitored index in the world, and S&P 500 index funds mimic the index with ETFs.

Index funds are established by a fund manager whose aim isn’t to outperform the market but rather mimic it. The only time the holdings in the index change are when the companies in the index change.

S&P 500 index funds include the 500 leading companies based on market capitalization in the U.S.

Pros

-

Minimal investment is required since you invest in the entire index, not individual securities.

-

You get an automatically diversified portfolio

-

The S&P 500 index has an average 10% return annually

-

They are passively managed and have minimal expense ratios

Cons

-

Companies are in the S&P 500 based on their market weight; if one industry is heavily weighted, such as technology, that industry could affect the index as a whole

-

You can’t exclude specific equities since the investment reflects the entire market

-

You can’t overcome the market

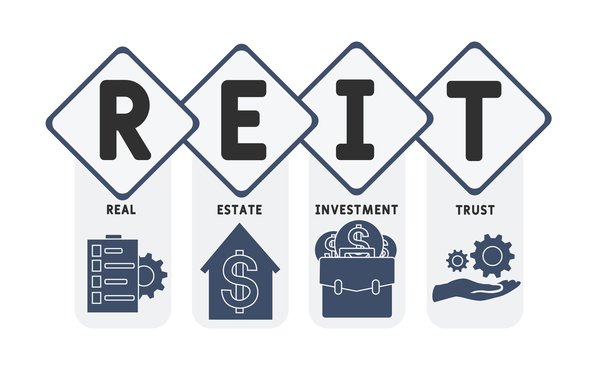

4. REIT Index Funds

REIT index funds enable investors to invest in real estate without possessing it directly. REITs are funds invested in real estate companies that, when publicly traded, include equities encompassing various sectors, such as apartment complexes, office buildings, and retail centers.

They pay dividends on 90% or more of their profits because they aren’t taxed at the corporate level. REITs often appreciate over time, allowing for capital appreciation and further benefits. Like any investment, they have volatility and should be considered a long-term investment.

Pros

-

Offers two methods to collect earnings, including capital appreciation and dividends

-

Low barrier to entry allowing even novice investors an opportunity to invest in real estate

-

Offers diversification away from the traditional stock market

Cons

-

REIT dividends are taxed as conventional income for investors

-

Non-publicly traded REITs can have excessive fees and minimal liquidity

-

Could be subject to market patterns

Read Also: 4 Ways to Make the Most of Your Investments This Year

5. Series I Bonds

Series I bonds are US Treasury-issued bonds that provide inflation protection. The bonds have a base interest rate posted and then add to it based on the current inflation rates.

In brief, the bond’s rates rise and decline with inflation, so if inflation goes up, the interest rates increase, and if inflation decreases, interest rates fall.

Series I bonds are another excellent way to diversify an aggressive portfolio because they have little to no risk of default. However, you can only set aside an annual limit of $10,000 per investor in Series I Bonds.

Pros

-

I Bonds fluctuate with inflation and, even without inflation, often pay greater rates than other conservative investments like HYSAs

-

Offers some tax benefits such as deferring interest payments until maturity or using the earned income for college (for qualified taxpayers)

-

There’s little to no risk of default

Cons

-

There’s an annual limit anyone is permitted to purchase ($10,000 per year plus up to $5,000 of your tax refund if applicable)

-

The only location to purchase them is the U.S. Treasury website which isn’t user-friendly

-

You must monitor the investment yourself since you don’t go through a broker to purchase them

.webp)