For decades, the Indian middle class held a "silent" fortune in kitchen cabinets and bank lockers. We’re talking about silver—vessels, heavy anklets, and coins passed down through generations. While gold was always the "emergency" asset, silver was just... there. That changed on April 1, 2026. With the RBI’s latest regulatory shift, Loans Against Silver 2026 has moved from a niche unorganized market experiment to a full-blown financial product. If you have silver, you now have a low-interest credit line. It’s that simple.

Key Takeaways

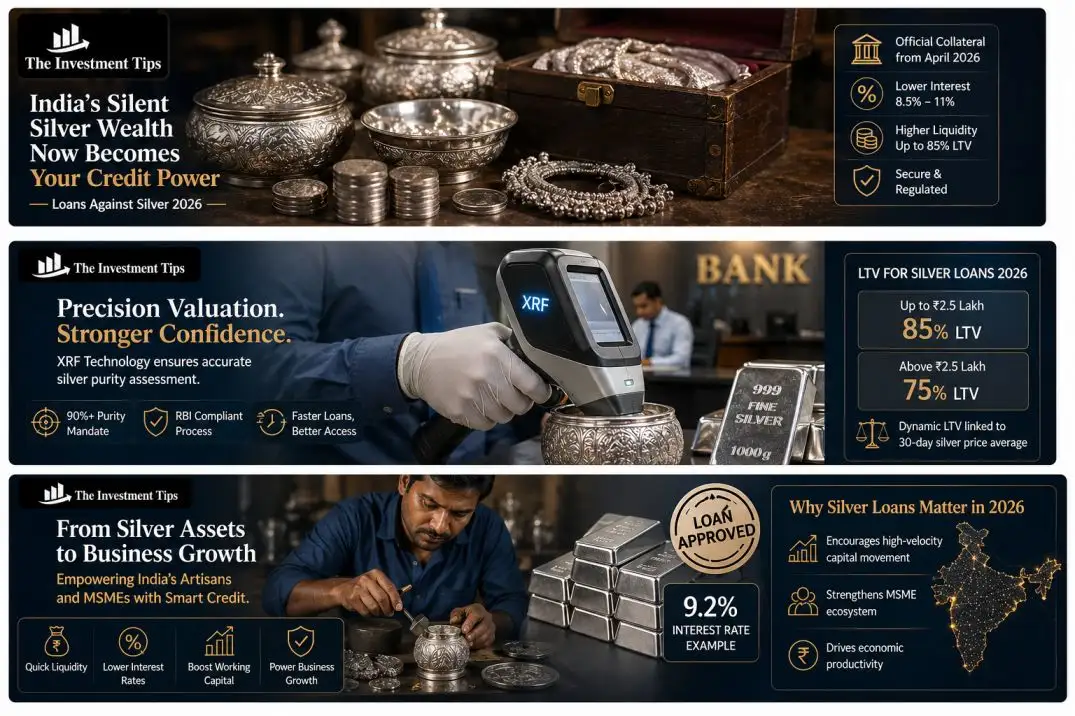

- The Pivot: Silver is now recognized as official collateral for retail and MSE loans as of April 2026.

- LTV Ratios: Expect an LTV for silver loans 2026 to hover around 75-85% for most PSU and private banks.

- Cost of Capital: Silver loan interest rates are significantly lower than personal loans, typically ranging from 8.5% to 11%.

- Purity Mandate: Only silver with a fineness of 900 (90%) or higher is generally accepted for pledging.

The Seismic Shift: Why Silver, Why Now?

The Indian gold loan market is saturated. Lenders were looking for the next big collateral pool, and they found it in our storage trunks. By formalizing algorithmic trading India styles of valuation for silver, the RBI has unlocked billions in "dead capital."

The Real-World Scenario: The Jaipur Artisan

Take Rajesh, a boutique silver jewelry exporter in Jaipur. In 2024, if Rajesh needed an urgent â‚ą3 lakh for raw materials, he had to pledge his family gold or take a 16% personal loan. His 15kg of silver inventory was "useless" to banks. Fast forward to mid-2026: Rajesh walks into a branch, pledges his silver bars, and secures a 9.2% interest loan in ninety minutes. Same assets, different era.

The Counter-Intuitive 'Hot Take'

Silver loans are actually better for the economy than gold loans. Why? Because gold is often held for sentimental "never-sell" reasons, leading to stagnant portfolios. Silver is more industrial. By allowing silver to be pledged, the RBI is encouraging high-velocity movement in the MSME sector. It's not just a loan; it's a productivity booster.

Pro-Tip: The "90% Rule" Most banks won't touch "German Silver" or low-purity alloys. Before you head to the bank, check the "fineness" mark. You need 900 or 925 (Sterling) to get the best LTV. If it’s not marked, expect the bank’s XRF machine to be ruthless.

Deep Dive: LTV for Silver Loans 2026

The Loan-to-Value (LTV) ratio is the heartbeat of any secured loan. In the world of silver collateral vs gold loan, the rules are tighter because silver is historically more volatile than its yellow cousin.

Technical 'Under-the-Hood' Details

Banks don't just look at the spot price. They use a 30-day moving average of the LBMA (London Bullion Market Association) silver price. To buffer against silver's famous price swings (where it can drop 5% in a day), the RBI has mandated a dynamic LTV.

- For loans up to â‚ą2.5 Lakh: Up to 85% LTV.

- For loans above â‚ą2.5 Lakh: Usually capped at 75%.

Silver Collateral vs Gold Loan: The Duel

While gold gets you higher LTV (often up to 90% in special schemes), silver is catching up. The main difference? The "Storage Factor." 10 Lakhs worth of gold fits in a pocket. 10 Lakhs worth of silver requires a sturdy box. Our banks have spent the last six months upgrading their strong-room floor reinforcement specifically for this.

Crunching the Numbers: Silver Loan Interest Rates

Why would you pledge your silver instead of just taking a credit card loan? Simple: the math. Silver loan interest rates are currently a steal.

|

Feature |

Silver Loan (2026) |

Personal Loan |

|

Interest Rate |

8.5% - 11% |

13% - 21% |

|

Processing Time |

1 - 3 Hours |

24 - 48 Hours |

|

Credit Score Impact |

Low (Secured) |

High (Unsecured) |

|

Prepayment Penalty |

Zero (RBI Mandate) |

2% - 4% |

The "Volatility Premium"

Wait. If silver is volatile, why is the interest low? Because the bank holds the physical metal. If the price of silver crashes, the bank makes a "Margin Call." You either pay more cash or they sell your silver. It’s a zero-risk game for them, which means a lower rate for you.

Pro-Tip: The Repayment Trap Always opt for "Overdraft" silver loans if you are a business owner. You only pay interest on the amount you use, not the whole limit. It’s like having a credit card with an 8% interest rate.

The Leaderboard: Best Banks for Silver Loans India

Not all banks have embraced the silver rush equally. If you are looking for the best banks for silver loans India, you need to look at who has the best XRF testing infrastructure.

The Top Contenders

- State Bank of India (SBI): The "Silver Rakshak" scheme offers the lowest rates but has the strictest purity checks.

- Federal Bank: Known for their "Digital Silver" integration where you can track your collateral value in real-time on an app.

- Muthoot Finance: The pivot king. They’ve converted 40% of their urban branches to handle bulk silver storage.

The Technical 'Glitches'

The biggest hurdle right now isn't the law; it's the valuation. Gold testing is standardized. Silver testing (especially for large vessels) is tricky. We are seeing banks adopt X-Ray Fluorescence (XRF) technology to check purity without drilling holes in your grandmother's silver plate.

Frequently Asked Questions (FAQ)

What is the maximum loan amount I can get against silver?

Most retail banks cap silver loans at â‚ą25 Lakhs per individual, though MSME categories can go higher depending on the business turnover and collateral volume.

Can I pledge silver utensils for a loan?

Yes, provided they meet the 90% purity mark. Most "Pooja" items in India are high-purity, while older "German Silver" or silver-plated items are usually rejected.

How is the silver price calculated for the loan?

Banks use the average closing price of silver (999 fineness) for the preceding 30 days as declared by the India Bullion and Jewellers Association (IBJA).

Is a silver loan better than a gold loan?

It depends on your inventory. If you have "d.ead" silver assets, it’s better because it leaves your gold (which has higher appreciation potential) untouched for larger future emergencies.

The Final Word: Your Legal Shield

In the 2026 trading environment, a "log" isn't just a text file on your hard drive; it is a forensic record of your compliance with federal mandates. Under the SEBI framework effective April 1, 2026, every automated order is treated with the same level of scrutiny as institutional trades.

When you apply for Loans Against Silver 2026, treat it with the same discipline. Keep your purity certificates. Log your valuation dates. If the bank ever disputes the value of your collateral during a price dip, your independent purity report is your only "legal shield."

Pro-Tip: The "Hallmark" Advantage Starting June 2026, silver hallmarking is expected to become mandatory for loans. If you’re buying silver today, get the HUID (Hallmark Unique Identification). It will make your loan process 5x faster next year