The Indian digital banking world just hit a massive reset button. If you’ve tried to send money recently and faced an unexpected "Transaction Failed" screen or a clunky new biometric prompt, you aren't alone. As of April 1, 2026, the Reserve Bank of India (RBI) has rolled out the most aggressive security overhaul in the history of the Unified Payments Interface.

The New UPI Rules April 2026 aren't just about changing limits; they are about killing the insecure SMS OTP and forcing every bank—from SBI to HDFC—to adopt a "Fiduciary Security" model. If you don't adapt, your digital wallet is essentially a paperweight.

Key Takeaways: The April 2026 Shift

- The Death of OTP: SMS-based verification is being phased out for high-value transfers in favor of device-bound biometrics.

- Transaction Caps: While the â‚ą1 lakh limit holds for most, specific sectors like Education and IPOs now allow up to â‚ą5 lakh.

- Merchant Fees: P2P (friend-to-friend) remains free, but some merchant transactions over â‚ą2,000 now carry an interchange fee.

- Verification: Always verify your receiver's identity via the new "Pre-Transaction Name Display" mandate.

The Friction Point: Why "New UPI Rules April 2026 India" Matter Now

For years, we’ve relied on a simple PIN and a shaky SMS OTP. It worked—until the phishers caught up. In 2026, the RBI decided that "convenience" was no longer worth the "fraud risk." Under the new New UPI Rules April 2026 India, every digital payment must now pass through Additional Factor Authentication (AFA).

The "Multi-Factor" Reality

Instead of just "Something you know" (your PIN), the system now demands "Something you are" (FaceID or Fingerprint) or "Something you have" (a hardware-bound device token). This is why your New UPI rules April 2026 SBI app might suddenly ask for a thumbprint even for routine transfers.

You may also read :- Types of Banking in India: A Complete Guide to Banking System

A Real-World Scenario: The "First-Time" Delay

Imagine you’re trying to pay a new landlord â‚ą25,000. Previously, it was instant. Now, under the 2026 mandate, your first transfer to a new beneficiary above â‚ą10,000 might face a 60-minute cooling-off window. It’s annoying, but it’s the only thing standing between you and a "Lookalike" scammer.

Pro-Tip: Update Your Biometrics. If your banking app (especially HDFC or SBI) keeps failing, it’s likely because your device-binding is outdated. Re-register your biometrics within the app settings to sync with the new 2026 encryption standards.

The Indian digital banking world just hit a massive reset button. If you’ve tried to send money recently and faced an unexpected "Transaction Failed" screen or a clunky new biometric prompt, you aren't alone. As of April 1, 2026, the Reserve Bank of India (RBI) has rolled out the most aggressive security overhaul in the history of the Unified Payments Interface.

The New UPI Rules April 2026 aren't just about changing limits; they are about killing the insecure SMS OTP and forcing every bank—from SBI to HDFC—to adopt a "Fiduciary Security" model. If you don't adapt, your digital wallet is essentially a paperweight.

Key Takeaways: The April 2026 Shift

- The Death of OTP: SMS-based verification is being phased out for high-value transfers in favor of device-bound biometrics.

- Transaction Caps: While the â‚ą1 lakh limit holds for most, specific sectors like Education and IPOs now allow up to â‚ą5 lakh.

- Merchant Fees: P2P (friend-to-friend) remains free, but some merchant transactions over â‚ą2,000 now carry an interchange fee.

- Verification: Always verify your receiver's identity via the new "Pre-Transaction Name Display" mandate.

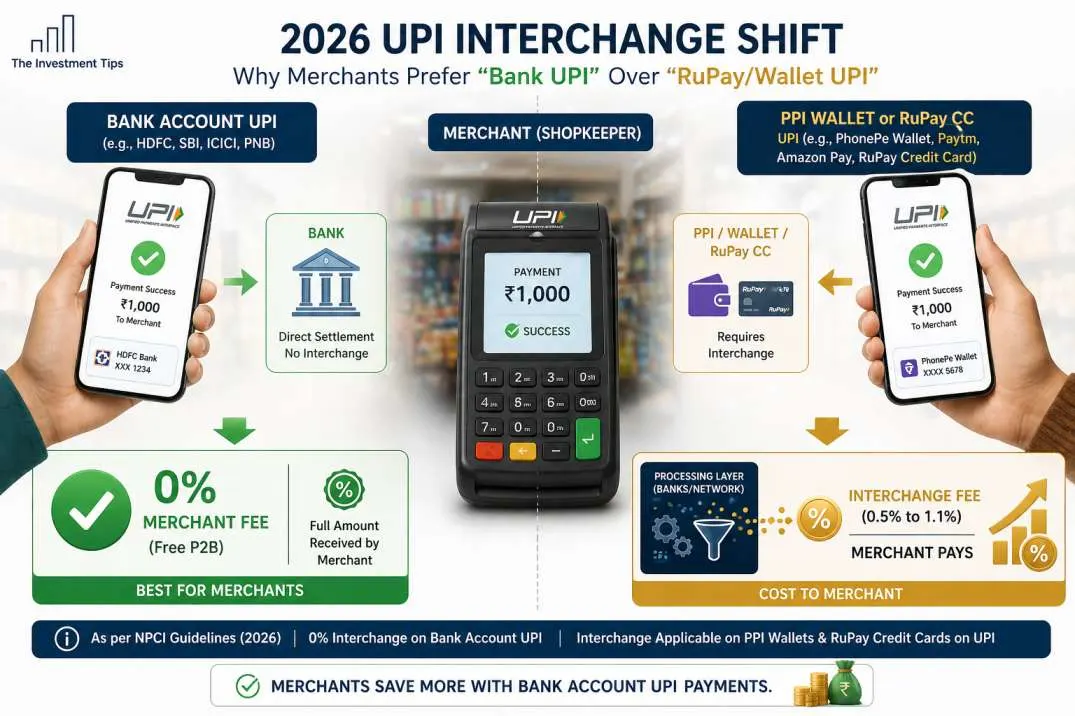

The Cost: UPI Transaction Charges from 1st April 2026

Is UPI still free? The answer is "Yes, but..." and that "but" is where the UPI transaction charges from 1st April 2026 come into play.

Technical "Under-the-Hood": The Interchange Shift

If you are sending â‚ą500 to your friend for dinner, it is 0% charge. However, if you use a Prepaid Payment Instrument (PPI) like a digital wallet (Paytm/PhonePe Wallet) or a RuPay Credit Card to pay a merchant more than â‚ą2,000, an interchange fee of 0.5% to 1.1% is applied.

Who Pays?

The customer never pays this fee directly. The merchant pays it to the service provider. However, don't be surprised if small shopkeepers start asking you to pay via "Bank Account UPI" instead of "Wallet UPI" to avoid these costs.

|

Merchant Category |

Interchange Fee (%) |

|

Fuel & Utilities |

0.5% - 0.7% |

|

Supermarkets |

0.9% |

|

Insurance & Mutual Funds |

1.1% |

|

P2P (Friend to Friend) |

0% (Always Free) |

The Indian digital banking world just hit a massive reset button. If you’ve tried to send money recently and faced an unexpected "Transaction Failed" screen or a clunky new biometric prompt, you aren't alone. As of April 1, 2026, the Reserve Bank of India (RBI) has rolled out the most aggressive security overhaul in the history of the Unified Payments Interface.

The New UPI Rules April 2026 aren't just about changing limits; they are about killing the insecure SMS OTP and forcing every bank—from SBI to HDFC—to adopt a "Fiduciary Security" model. If you don't adapt, your digital wallet is essentially a paperweight.

Key Takeaways: The April 2026 Shift

- The Death of OTP: SMS-based verification is being phased out for high-value transfers in favor of device-bound biometrics.

- Transaction Caps: While the â‚ą1 lakh limit holds for most, specific sectors like Education and IPOs now allow up to â‚ą5 lakh.

- Merchant Fees: P2P (friend-to-friend) remains free, but some merchant transactions over â‚ą2,000 now carry an interchange fee.

- Verification: Always verify your receiver's identity via the new "Pre-Transaction Name Display" mandate.

The Limits: UPI Transaction Limit from 1st April 2026

There is a lot of noise about how much you can actually send. Let’s clear the air. The UPI transaction limit from 1st April 2026 is no longer a "one size fits all" number. It’s now categorized by the "Risk Level" of the transaction.

The 2026 Limit Hierarchy:

- Standard P2P/P2M: â‚ą1 Lakh per day (remains the baseline for most).

- Capital Markets & IPOs: Boosted to â‚ą5 Lakh to support retail investors.

- Education & Healthcare: Verified institutions now allow up to â‚ą5 Lakh to prevent credit card debt for essential services.

- UPI 123Pay (Feature Phones): Doubled to â‚ą10,000 per transaction to help rural adoption.

The Hot Take: "Unlimited" is a Lie

Some fintechs claim "unlimited" transfers if you use their "Pro" versions. This is marketing fluff. Regardless of the app, your New UPI rules April 2026 HDFC or ICICI account is still bound by the NPCI's daily volume cap (usually 20 transactions per day). If you hit that wall, no amount of "Premium" subscription will help you.

The "Failed SIP" Crisis: E-Mandates in 2026

If your Mutual Fund SIP or Netflix subscription bounced this month, blame the new e-mandate rules. RBI now requires a "Pre-Debit Notification" 24 hours before the money leaves your account. If your bank fails to send that SMS/Email, the transaction is auto-blocked.

Case Study: The â‚ą15,000 Threshold

We saw a massive surge in failed transactions for premium insurance payments. Why? Because any recurring payment above â‚ą15,000 (up to â‚ą1 Lakh) now requires a one-time additional factor authentication every single time. It is no longer "set it and forget it." You have to "approve" the high-value debit every month.

FAQs

Q: Why is my SBI app suddenly obsessed with my fingerprint?

A: You can thank the New UPI rules April 2026 SBI rollout for that. RBI finally killed the "OTP-only" era because scammers were getting too good at intercepting SMS. Now, biometrics are the "Additional Factor of Authentication" (AFA). It’s annoying for five seconds, but it ensures that even if someone swipes your phone, they can't swipe your life savings.

Q: I keep hearing about "hidden" UPI transaction charges from 1st April 2026. What gives?

A: If you’re just sending money to your mom or splitting a bill with friends, it is still â‚ą0. Charges only kick in for merchants (not you) when they accept payments over â‚ą2,000 via "Wallets" or RuPay credit cards. P2P (Peer-to-Peer) bank transfers remain the crown jewel of free banking in India.

Q: My HDFC UPI limit is capped at â‚ą5,000. Is my account blocked?

A: Not at all. Under the New UPI rules April 2026 HDFC and industry-wide norms, any "Fresh Registration" or SIM-swap triggers a 24-hour "cool-off" period. You're restricted to â‚ą5,000 for the first day as a safety net against digital hijackers. Think of it as a mandatory speed-bump while the bank verifies it's actually you.

Q: My SIP failed this morning. Is it because of the new rules?

A: Likely. One of the quietest New UPI rules April 2026 India shifts is the "Off-Peak" processing mandate. Auto-debits now happen during non-peak hours (before 10 AM or after 9:30 PM). If your bank's server had a hiccup during that window, the mandate fails. You might need to manually re-authorize your first high-value SIP under the new 2026 e-mandate protocols.

Final Verdict: Survival of the Safest

The New UPI Rules April 2026 represent a painful but necessary evolution. We are moving away from the "OTP Era" and into the "Biometric Era." While the "Linguistic Friction" of terms like Additional Factor Authentication might sound like banking jargon, the reality is simple: your money is now locked behind a wall that only you can open.

Update your apps, sync your biometrics, and watch those SIP notifications. It works. Until you ignore the new mandates—then your payments simply won't. Stay sharp.

in India.webp)