.webp)

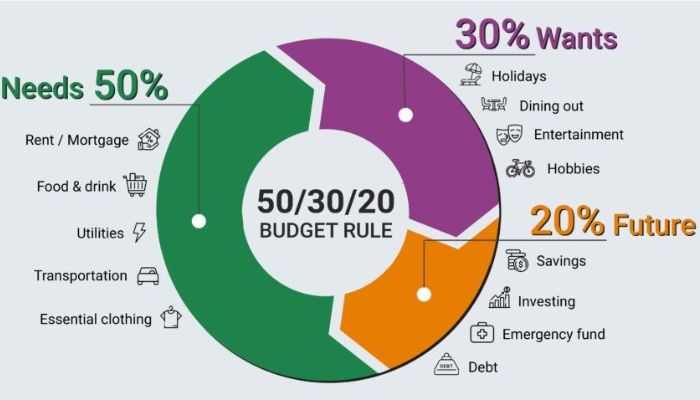

I cracked open my first salary slip years ago and realized nobody teaches us how to actually manage money in India. That is exactly why the 50/30/20 budget rule in India works so brilliantly for our generation. It is a highly practical formula where you take your monthly take-home salary and split it into three incredibly clear buckets. You put 50% toward your absolute survival needs like your house rent, electricity bills, and monthly groceries.

Then, you can comfortably spend 30% on your personal wants like weekend dining out, shopping, and travel without feeling any guilt. Finally, you lock away the remaining 20% for your future savings, emergency funds, and long-term investments. This simple framework gives Indian earners a stress-free path to build wealth while living a great lifestyle today.

What is the 50/30/20 budget rule?

Managing money often feels highly confusing when you lack a clear, structured system. Many young professionals struggle to save a single rupee because they never track their daily cash flow. This simple financial guideline offers an incredibly practical solution to organize your personal finances.

Elizabeth Warren, a well-known bankruptcy expert, originally created this simple formula to help working families organize their money. You do not need to master complex accounting software or hire an expensive advisor to use this method.

The 50/30/20 budget rule explained simply means dividing your total net income into three distinct parts. Your net income refers to the actual money that enters your bank account after all taxes and pension deductions. Once you know this exact monthly figure, you can easily allocate your funds to secure your financial future.

You may also read :- Best Saving Schemes in India 2026: Highest Interest Rates and Rules

Breaking Down the 50% Category: Your Essential Needs

The largest portion of your monthly paycheck goes directly toward the absolute essentials that keep your household running. Under the 50/30/20 budget rule india, your needs represent the non-negotiable costs that you must pay to survive.

Rent and Home Loans in Urban Centers

Whether you reside in a bustling metro area or a smaller town, housing represents your single largest monthly expenditure. This specific bucket covers your monthly rent payments or your home loan repayments. You must prioritize these housing payments to ensure you always have a secure place to live.

Electricity, Water, and Daily Travel

Your basic utility bills, high-speed internet connections, and cooking gas expenses belong to this essential group. Additionally, the money you spend on petrol for your vehicle, or your monthly train and bus passes, falls under your necessary survival expenses.

Grocery Bills and Medical Coverage

Basic food items, fresh vegetables, and monthly household supplies are essential for your physical survival. You should also place your regular prescription medicines and your monthly health insurance premiums in this 50% bucket to protect your family from unexpected crises.

Exploring the 30% Category: Your Personal Wants

The second bucket lets you enjoy your hard-earned salary today without experiencing any financial guilt. This section covers your personal lifestyle choices, which are nice to have but are not strictly necessary to live.

Dining Out and Online Food Apps

Ordering food through mobile apps or hanging out at local cafes on weekends fits right here. You must eat to live, but buying expensive coffees and fancy restaurant meals are lifestyle choices that belong in your fun budget.

Media Subscriptions and Weekend Fun

Your monthly streaming platforms, movie tickets, weekend outings, and music subscriptions fit perfectly here. These leisure items keep your life fun, but you can instantly cancel them if you experience a sudden loss of income.

Wardrobe Upgrades and Holiday Trips

Splurging on festive clothes, swapping a perfectly fine phone for the latest shiny model, or booking impromptu mountain trips—all of this sits right here. Tracking this fluid bucket ensures your lifestyle choices never accidentally outpace your actual paycheck.

Analyzing the 20% Category: Future Savings and Investments

The final portion of your income secures your long-term wealth and protects your family during tough times. Many seasoned financial planners advise treating this 20% portion as a bill that you pay directly to your future self on payday.

Creating a Robust Emergency Fund

Before you start purchasing shares or mutual funds, you must establish a secure cash buffer. You should accumulate at least six months of living expenses in a simple savings account to survive potential layoffs or medical issues.

Investing in Long Term Growth

Once you establish your emergency fund, you can direct this 20% portion toward building your wealth. This path includes starting monthly systematic investment plans in equity funds, depositing money in public provident funds, or contributing to retirement schemes.

Clearing High Interest Debt

If you carry expensive credit card balances or personal loans, you should use this savings bucket to make extra payments. Eliminating high-interest debt quickly saves you a massive amount of money and improves your overall financial peace of mind.

How to Apply the 50/30/20 budget rule india in Real Life?

Applying this financial rule successfully requires an honest look at your current daily spending habits. You can start by reviewing your bank statements from the past three months to understand where your money actually goes.

Calculate Your Actual Income

Identify the exact amount of money that lands in your bank account every month. Do not count unpredictable yearly bonuses or festive incentives unless you already have them in your hand. Use this stable net salary to calculate your exact target categories.

Sort and Categorize Every Expense

Divide your recent monthly spending into needs, wants, and savings. You might discover that your entertainment choices consume over half of your income while your savings remain empty. This clear realization helps you adjust your daily habits.

Adjust the Proportions for high-cost locations.

If you reside in an expensive city, your monthly rent might consume a massive portion of your income. You can temporarily adjust your targets to 60/20/20 while you search for ways to reduce your expenses or increase your monthly earnings.

Why This Simple Money Strategy Works Wonders for Indian Earners?

The local economy is growing at a rapid pace, and lifestyle expenses are climbing very quickly for young professionals. This easy framework provides a highly practical solution that balances your current happiness with your future financial security.

"The primary benefit of this budgeting system lies in its extreme simplicity. It removes the daily pressure of tracking every single rupee and guides you to manage your money using three broad, clear categories." — Vijay Kumar, Certified Financial Planner

By automating your savings immediately after your salary arrives, you eliminate the temptation to spend your cash on impulsive lifestyle choices. It creates a powerful habit that easily adapts as your career progresses and your salary rises over time.

Common Challenges and Solutions for Indian Households

No financial plan is perfect, and you will definitely hit a few speed bumps when you try to follow it in real life. The secret is knowing how to handle these sudden twists and turns so you do not completely lose track of your money when unexpected bills show up in the middle of the month.

- Rising Costs of Living: Education and medical costs are rising rapidly. You should review your budget twice a year to ensure your basic needs category still covers your actual survival expenses.

- Huge Festive Expenses: Major celebrations and family weddings can easily break your monthly plan. You should set aside a small portion of your 30% wants bucket throughout the year to build a dedicated festive fund.

- Social Comparison: Online platforms often tempt people to buy premium items to impress others. You must stay focused on your personal goals and remember that saving money today guarantees a relaxed tomorrow.

Using a 50 30 20 budget rule india calculator for Fast Results

You do not need to build highly complex spreadsheets to manage your household cash flow. A basic 50 30 20 budget rule india calculator helps you discover your exact target numbers within just a few seconds.

| Monthly Net Income | 50% Essential Needs | 30% Personal Wants | 20% Future Savings |

| â‚ą50,000 | â‚ą25,000 | â‚ą15,000 | â‚ą10,000 |

| â‚ą80,000 | â‚ą40,000 | â‚ą24,000 | â‚ą16,000 |

| â‚ą1,00,000 | â‚ą50,000 | â‚ą30,000 | â‚ą20,000 |

You can use these clear targets to review your actual bank statements. If your current savings fall far below the 20% mark, look for immediate ways to trim your lifestyle expenses to protect your future.

Final Thoughts on Achieving Financial Freedom

Using the 50/30/20 budget rule india helps you establish a highly secure financial path without giving up the lifestyle choices that bring you joy. It removes the stress from your personal spending because you already know your future savings and monthly bills are fully covered. Start with small adjustments, automate your investment transactions, and watch your personal wealth grow steadily over the years.

Frequently Asked Questions

What should I do if my essential bills exceed 50% of my monthly salary?

If you live in a highly expensive metropolitan area, your basic rent and transport costs might exceed half of your paycheck. You should search for ways to reduce your lifestyle spending, find a roommate to share housing costs, or look for opportunities to increase your primary income.

Do my provident fund contributions count toward the 20% savings category?

Yes, your monthly contributions to public provident funds and employee provident funds are highly secure long-term investments. You should include these specific amounts in your 20% savings bucket alongside your mutual fund investments and emergency savings.

Can I modify these percentages to target my personal goals?

Absolutely. This budgeting framework is highly flexible to suit your changing life stages. If your primary goal is to retire early, you can easily shift to a 40/20/40 structure, where you save 40% of your earnings and reduce your wants to 20%.

Should I pay off my home loan using my savings or needs category?

Your regular monthly home loan repayment represents a non-negotiable commitment, which belongs in your 50% essential needs category. However, if you want to make extra payments to clear the loan early, you should use money from your 20% savings category.

.webp)