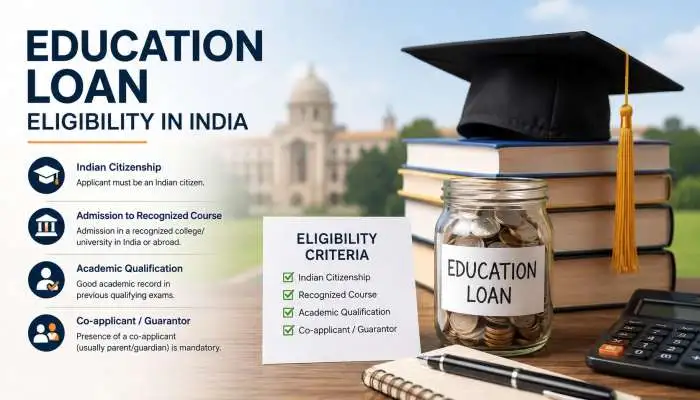

You’ve cleared your 12th—or you’re about to. Your board results are either a source of pride or a mild heart attack. And now someone told you that you need to understand education loan eligibility in India before any bank even looks at your application. Truth? Most students get rejected not because they’re "unworthy," but because they walked in blind.

We’ve spent years watching banks approve loans for the least deserving profiles while rejecting brilliant students over tiny technicalities. Frustrating? Absolutely. Fixable? One hundred percent.

This guide isn’t your typical “7 easy steps” fluff. We’re going deep—into collateral traps, percentage cutoffs, government schemes nobody uses (but should), and the exact moment you become “eligible” in a banker’s eyes.

The Four Pillars That Decide Your Fate

Before we talk about specific banks or government programs, you need to understand how lenders think. A loan officer doesn’t see your dream. They see risk.

Four things matter:

- Your academic track record (marks, entrance exams, board scores)

- The course and institution’s reputation (IIT vs. no-name private college)

- Co-applicant’s financial health (parents’ income, existing loans)

- Collateral or lack thereof (property, fixed deposits, or… nothing)

Change any one of these, and your education loan eligibility in India shifts dramatically. We’ve seen a 65% scorer get a â‚ą40 lakh loan because their dad was a government employee. We’ve also seen a 92% scorer get rejected because the course was “too niche” and the bank couldn’t find resale value. Harsh? Maybe. But that’s the system.

You may also read :- How to Refinance Student Loans in 2026: A Step-by-Step Guide

Minimum Percentage Required for Education Loan in SBI – The Real Number

This is where most students get misled. Walk into any SBI branch, and the official brochure says, "50% aggregate in 12th for the general category.” Technically true. Practically useless.

For undergraduate courses after 12th:

- Engineering/Medical – 60%+ in PCM/PCB. Below that? Expect a co-applicant with strong income or collateral.

- Commerce/Arts – 55%+ minimum. But honestly? 65%+ makes the process smoother.

- Diploma/certificate courses – 50% works, but the loan amount gets capped (usually â‚ą4-7 lakhs).

For postgraduate courses:

-

They look at graduation marks more than 12th grade. But your 12th percentage still whispers in the background. Drop below 55% in 12th, and the internal credit score takes a hit.

One loan manager in Delhi told us off the record, "We approve 70% of applicants with 65% or more in 12th." That number falls to 30% for the 50-60% bracket. And for below 50%? Only if collateral is solid gold.” So when someone asks what percentage is required for an education loan in SBI, your answer isn’t a single number. It’s a sliding scale.

- Safe zone: 65%+

- Risky zone: 50-64%

- Red zone: Below 50% (don’t walk in without property papers)

But here’s a trick nobody tells you: SBI also considers improvement exams. Failed a subject? Gave compartment? They recalculate. We’ve had clients jump from 48% to 59% after reappearing for two subjects. Suddenly, “ineligible” became “maybe eligible.”

How to Get Education Loan After 12th – The Step-by-Step That Actually Works

You’re 17 or 18. You’ve never seen a sanction letter. EMIs sound like a foreign language. Relax. We’ll walk.

Step 1—Don't wait for the admission letter

Biggest rookie mistake. Students think: “I’ll get the college seat first, then the loan.”

Wrong sequence.

Start the loan process the day your 12th results are out. Even before you apply to colleges. Why? Because the bank’s “eligibility in principle” takes 7-10 days. If you wait until July, every other student is standing in the same line.

Step 2 – Choose your weapon: Secured vs. Unsecured loan

- Secured (collateral): Lower interest rate (SBI 8.5-9.5%), higher loan amount (â‚ą20 lakh+), and easier approval even with average marks.

- Unsecured (no collateral): Higher interest rate (11-14%), lower cap (usually â‚ą7.5 lakh for most banks), stricter percentage requirements.

Most students don’t know education loan eligibility without collateral exists, but the terms are brutal. We’ll get there in a minute.

Step 3 – Find a co-apparent who doesn’t have hidden debt

Parents are the obvious choice. But if your father already has a home loan + car loan + personal loan, his disposable income gets eaten before your EMI is even calculated.

Bankers look at “FOIR”—Fixed Obligation to Income Ratio. If your parents are already paying 50%+ of their income toward existing EMIs, your education loan won’t pass internal checks.

Step 4 – The document game (win it before you start)

Create a folder with:

- 12th mark sheets (and 10th, because banks ask)

- Entrance exam scorecard (JEE, NEET, CLAT, etc.)

- Provisional admission letter (even a conditional one works)

- Cost breakdown from college (fee structure, hostel, books)

- Co-applicant’s IT returns (last 2 years)

- Bank statements (last 6 months)

Missing even one? The file sits on someone’s desk for two weeks. Then you get a call: “Please submit document X.” Another week lost.

Step 5 – Apply to three banks simultaneously

Never put all hope in SBI. Also try Bank of Baroda, Canara Bank, and a couple of NBFCs (Avanse, HDFC Credila). Each has different education loan eligibility criteria in India. One might reject you for a percentage; another might approve based on the college’s ranking.

We’ve seen a student rejected by SBI and PNB but approved by Bank of India within 5 days. Same marks. Same college. Different internal policies.

Education Loan by Government – The Schemes You’re Probably Ignoring

When people say “government education loan,” most think of the Central Sector Interest Subsidy Scheme (CSIS). Important, but limited.

Let’s break down the real education loan by government options that actually help students like you.

1. PM Vidyalaxmi Scheme (launched 2024, expanded 2025)

This is the new kid on the block. And it’s surprisingly good.

- Eligibility: Admission to top 500 NIRF-ranked institutions (colleges are listed on the portal)

- Loan amount: Up to â‚ą10 lakh without collateral for some categories

- Benefit: Full interest subsidy during moratorium (study period + 1 year) for families with annual income under â‚ą4.5 lakh

Most students don’t check if their college is in the NIRF top 500. Do that first. If yes, you’re eligible for a zero-interest period that saves lakhs in compounding.

2. Central Sector Interest Subsidy Scheme (CSIS)

This is the older one. Still alive. Still useful.

- Income cap: Parental income under â‚ą4.5 lakh/year

- Loan limit: Up to â‚ą10 lakh

- Subsidy: Government pays interest during moratorium (but only for the first â‚ą10 lakh of the loan)

Here’s the catch nobody mentions: The subsidy doesn’t apply if you get a job within 6 months of finishing the course. Sounds good, right? No—because the moment you start earning, interest starts accruing from Day 1 of the loan. So you actually lose the benefit if you’re too successful. Irony.

3. State-Specific Schemes (Don’t ignore these)

Tamil Nadu has the Moovalur Ramamirtham Ammaiyar Higher Education Assurance Scheme. Maharashtra has an EBC (Economically Backward Classes) fee waiver. Kerala’s Susegrah scheme for professional courses.

These aren’t “loans” exactly. They’re fee reimbursements or interest subsidies tied to state domicile. But they work beautifully with a regular bank loan. Use them to reduce the principal amount you borrow.

4. Education Loan by Government via PSU Banks

This isn’t a separate scheme—it’s a mandate. Public sector banks (SBI, BOB, Canara, PNB, etc.) are required to offer education loans under the Indian Banks’ Association (IBA) Model Education Loan Scheme.

What does that mean for you?

- No prepayment penalty (you can pay early without fines)

- Moratorium period = course duration + 6 months (or 1 year after getting a job, whichever is earlier)

- Simple interest during moratorium (not compound, thank God)

But here’s the rub: The IBA scheme is a guideline, not a law. Banks interpret it loosely. So “no collateral up to â‚ą7.5 lakh” in the brochure becomes “we need a third-party guarantee” in reality. Push back when they add extra conditions.

Education Loan Eligibility Without Collateral – The Brutal Truth

This is the question we hear most: “I don’t own a house. My parents are tenants. Can I still get a loan?”

Short answer: Yes. Long answer: It’s a different ballgame.

Education loan eligibility without collateral is possible, but banks will squeeze you on three things:

A. Percentage becomes everything

No property to offer? Then your marks are your collateral. For unsecured loans:

- 70%+ in 12th = multiple offers

- 60-69% = limited options, higher interest

- Below 60% = almost impossible without a strong co-applicant income

B. Top colleges only

Banks have an “approved list” of institutions for unsecured loans. Think IITs, NITs, IIITs, and top law and medical colleges. If your college isn’t on that list, no collateral = no loan.

Ask the bank for their “A-list” of colleges before you apply. Don’t guess.

C. Co-applicant’s income becomes the real collateral

If you don’t have property, the bank will demand your co-applicant (usually a parent) earn at least â‚ą25,000-30,000/month for a â‚ą7.5 lakh loan. For higher amounts, they’ll want â‚ą50,000+ monthly income.

And here’s the kicker: Even with no collateral, some banks ask for a third-party guarantee—another person (relative, family friend) signing as a guarantor. That person’s assets become unofficial collateral. Legally, it’s different. Practically, it’s the same risk.

NBFCs are more flexible here. Avanse, HDFC Credila, and InCred—they do unsecured loans more willingly than PSU banks. Interest rates are higher (11-14% vs. SBI’s 8.5%), but approval rates are better for average marks and non-IIT colleges.

One student we advised – 62% in 12th, B.Com admission in a decent Mumbai college – got rejected by three PSU banks. Credila gave him â‚ą6 lakh in 10 days with his mother as a co-applicant (salary: â‚ą35k/month). He paid 12.5% interest. Was it ideal? No. Did he graduate? Yes.

Sometimes “good enough” beats “perfect.”

Hidden Factors That Kill Your Education Loan Eligibility (Even When You Have Great Marks)

Let’s talk about the silent killers.

Residence proof mismatches—Your 12th marksheet has one address. Your parent’s Aadhaar has another. The bank's KYC flags you. Fix it before applying.

Course duration exceeding 7 years – Some integrated courses (like dual degree or PhD integration) stretch to 8-9 years. Most PSU banks cap the moratorium at 7 years. After that, EMIs start even if you’re still studying. Read the fine print.

Part-time/distance courses – Zero eligibility in most banks. They only fund full-time, regular, classroom programs. Yes, even if it’s from a good university.

Two-word rejection reason: “Negative CIRIL score”—CIRIL is the credit bureau for education loans. If your co-applicant has defaulted on any loan ever – even a tiny credit card bill – your file gets a red flag. Check your parents’ credit score before applying.

Final Word: Eligibility Is Negotiable. Don’t Take the First No.

Here’s what we’ve learned from hundreds of cases. The published education loan eligibility criteria in India are a starting point, not a finish line. Banks have discretionary powers. Branch managers have targets. Loan officers have monthly approval quotas.

If one bank says no, ask why in writing. Then fix that specific reason. Low percentage? Offer a shorter repayment tenure. Weak co-applicant income? Bring a guarantor. Course not on the list? Ask for a “special approval” from the regional office.

And if you’re stuck? Government schemes like education loans by the government exist exactly for students who fall through the cracks. Use them. Fight for them.

Your marks are on paper. Your eligibility is in the details.

Frequently Asked Questions

Q1: Can I get an education loan without a co-applicant?

No. Every bank requires a co-applicant (parent or guardian) for students under 18. For adults, some NBFCs consider it, but interest rates jump to 15%+.

Q2: Does SBI give education loans for 50% in 12th?

Yes, but only with strong collateral or a high-income co-applicant. Without collateral, 60% is the unofficial floor.

Q3: How to get an education loan after 12th if admission is not confirmed yet?

Apply for a “pre-approved loan in principle” using your 12th marks and entrance exam score. Banks issue a conditional sanction letter valid for 3-6 months.

Q4: What is the maximum loan under education loan by government schemes?

PM Vidyalaxmi covers up to â‚ą10 lakh (interest subsidy). The actual loan can be higher from a bank; the government only subsidizes the first â‚ą10 lakh.

Q5: Education loan eligibility without collateral for studies abroad?

Very tough. Most foreign universities require collateral for loans above â‚ą20 lakh. Unsecured options exist (Prodigy Finance, MPower) but only for specific countries and courses.

Q6: What percentage is required for an education loan in SBI for an MBBS?

Minimum 60% in PCB. Government medical colleges get easier approval; private colleges need 65%+ or collateral.

Q7: Can I transfer my education loan to another bank?

Yes, after 1 year of repayment. It’s called “balance transfer.” A new bank pays off the old loan if they offer a lower interest rate.

Q8: What happens if my co-applicant dies during the loan period?

Most banks have a “co-applicant death” clause. A loan doesn’t get written off. You’ll need to bring a new co-applicant or convert to a personal loan at higher interest. Read your agreement’s fine print.

.webp)