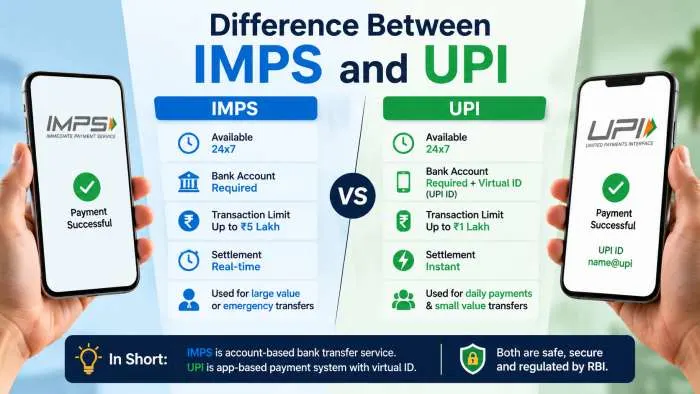

Think about how we deal with cash nowadays in India. Nobody wants to waste time standing in long lines at a bank branch anymore. We just pull out our phones. Most of the time, we rely on two main tools to shift our cash: IMPS and UPI. Now, if you look at the difference between imps and upi, it really comes down to the details you have to type in. With IMPS, you are doing an old-school bank transfer, so you need the actual account number and branch code.

UPI simplifies things by using a virtual ID or just a mobile number to send funds right away. That makes UPI perfect when you need to buy groceries quickly, while IMPS stays handy for sending huge chunks of money.

Understanding the Basics of Digital Payments

To pick the right tool, you first need to know what each one actually does.

What is IMPS (Immediate Payment Service)?

IMPS stands for Immediate Payment Service. The National Payments Corporation of India, or NPCI, brought this system to life in 2010. Before IMPS came along, people had to wait for bank working hours to send money. If you needed to transfer funds on a Sunday or a public holiday, you were simply out of luck.

IMPS changed all that completely. This service works every single day, at any hour. Whether it's 2 AM on a Tuesday or 10 PM on a Sunday, your money moves instantly.

Think of IMPS like a courier that delivers your money directly to the receiver's bank account. But here's the catch – you need the exact delivery address. That means you must know the receiver's bank account number and the IFSC code of their branch.

Once you have these details in hand, sending money becomes straightforward. You can do it through your bank's mobile app, log in to internet banking from your computer, or even use an ATM if that's more convenient for you.

You may also read :- New UPI Rules April 2026: Why Your Payments Are Failing and How to Fix It

What is UPI (Unified Payments Interface)?

UPI stands for Unified Payments Interface. NPCI launched this system in 2016. It was built on top of the IMPS infrastructure to make things even simpler . UPI is like sending a text message with money attached.

You create a Virtual Payment Address (VPA), like yourname@bank. You don't need to share your account number or IFSC code with anyone. You can also use QR codes or mobile numbers linked to a bank account to make payments . This makes UPI very easy for everyday use, like paying for vegetables, groceries, or auto-rickshaw rides.

The Main Difference between imps and upi

The biggest Difference between imps and upi lies in how you identify the person you are paying.

How IMPS Works

With IMPS, the transaction is like a traditional bank transfer. You must log in to your bank's app or website. You add the beneficiary by entering their name, account number, and IFSC code. Some banks require you to wait a few hours to activate the new beneficiary for security reasons . Then, you enter the amount and confirm with a One-Time Password (OTP) or MPIN . The money reaches the other account instantly.

How UPI Works

UPI works through a mobile app like Google Pay, PhonePe, Paytm, or your bank's own app. You don't need to add the beneficiary beforehand. You just enter the receiver's UPI ID, scan a QR code, or select their mobile number . You enter the amount and your UPI PIN. The money is then instantly transferred. The process is fast, simple, and works in just a few taps .

Key Transaction Methods

| Feature | IMPS | UPI |

|---|---|---|

| Identification | Account Number + IFSC Code, or MMID | Virtual Payment Address (VPA), QR Code, or Mobile Number |

| Beneficiary Setup | Needs to be added and often activated | No prior registration needed |

| Process | More steps, traditional banking style | Fast, simple, like sending a message |

Head-to-Head Comparison: Speed, Limits, and Costs

Let's break down the other important factors to consider.

Which is faster, UPI or IMPS?

Both systems offer real-time fund transfers. So, the answer to "Which is faster, UPI or IMPS?" is that they are both very fast. However, UPI feels faster because it has fewer steps. You don't have to wait for beneficiary activation. You just scan, tap, and go. The backend technology is similar, but the user experience makes UPI quicker for most people.

Transaction Limits: How Much Can You Send?

There is a big difference in how much money you can send.

- IMPS: This service generally allows for higher transaction limits. The standard limit is often up to â‚ą5 lakh per day . This makes it suitable for sending larger sums of money, like paying a supplier or transferring rent.

- UPI: The standard limit for UPI is usually â‚ą1 lakh per transaction . For certain special cases like tax payments or IPO applications, this limit can be higher, but for everyday person-to-person transfers, â‚ą1 lakh is the cap .

Charges and Fees: IMPS vs UPI

Cost is another important factor.

- IMPS: Banks usually charge a small fee for IMPS transactions. This fee can range from â‚ą1 to â‚ą25, depending on the bank and the amount you are transferring .

- UPI: UPI transactions are mostly free for individual users . This is a major reason for its immense popularity. You can send money to friends or pay a merchant without worrying about extra charges.

Pros and Cons of Each System

Every payment method has its strengths and weaknesses.

Advantages of IMPS

Higher Limits: Perfect for large money transfers. If you need to send more than â‚ą1 lakh, IMPS is a good choice.

Works Without Internet: Some banks offer IMPS via SMS, which can work even on basic phones without a smartphone .

Direct Bank Transfers: It's a direct, bank-to-bank system. Some people find this more reassuring for large amounts.

More Access Channels: You can use it through mobile apps, net banking, ATMs, and even bank branches .

Disadvantages of IMPS

Requires Bank Details: You need to know the recipient's account number and IFSC code . This can be time-consuming if you don't have the details handy.

Potential Charges: Most banks charge a fee for this service .

Less User-Friendly: The process of adding a beneficiary and entering all the details makes it less convenient for small, daily purchases.

Advantages of UPI

Super Simple: You only need a UPI ID or QR code. No bank details are required, which is great for privacy and convenience .

Free to Use: There are usually no fees for transferring money using UPI .

Versatile: Beyond sending money, you can pay bills, book tickets, buy insurance, and even request money from others .

Widely Accepted: Almost every shop, big or small, accepts UPI payments through QR codes .

Disadvantages of UPI

Lower Limits: You generally cannot send more than â‚ą1 lakh per day .

Needs Internet Connection: UPI primarily works through mobile apps that require a stable internet connection .

Possible Failures: Sometimes transactions fail during peak hours or due to server issues . While the money is usually refunded, it can be inconvenient.

Security Showdown: Is IMPS Safer Than UPI?

A common question is, " Is IMPS safer than UPI?" The answer is that both are highly secure.

- IMPS: It uses bank-level security. When you add a beneficiary, you are verifying a specific bank account. You need to enter an OTP or MPIN to complete the transfer . This adds a layer of verification.

- UPI: It uses two-factor authentication. This means your mobile device (which is bound to your bank account) and your UPI PIN are both needed to make a transfer . Your bank details are hidden from the receiver, which is a privacy plus.

The policy researcher and corporate advisor Srinath Sridharan says, “UPI offers a far superior user experience, an open app ecosystem, QR code ubiquity, and continuous innovation..." .

The choice is about your comfort level. If you feel safer entering a bank account number for a large sum, choose IMPS. For everyday small payments, UPI is perfectly safe and secure. "Both are secure and regulated by RBI. UPI simplifies the process, while IMPS sticks to traditional banking security" .

When to Choose IMPS vs UPI

So, which one should you use? It depends on what you need to do.

Best Use Cases for IMPS

- Paying Your Supplier: If you run a business and need to pay a vendor â‚ą50,000 or more, IMPS is a good option .

- Paying Your Rent: If your monthly rent is more than â‚ą1 lakh, you will need to use IMPS to make the transfer .

- Emergency Transfers: Sometimes, UPI can have technical glitches. If a UPI transaction fails and you don't want to wait, IMPS can be a reliable backup .

- Paying Without a Smartphone: If you are in an area with no internet and have a basic phone, you might be able to use IMPS via SMS .

Best Use Cases for UPI

- Daily Shopping: Buying vegetables, paying for groceries, or eating out? UPI is the quickest and easiest way to pay.

- Splitting Bills: You can instantly send your share of a dinner or movie ticket to a friend using their UPI ID.

- Merchant Payments: Every shopkeeper with a QR code accepts UPI. It's the most common method for retail purchases .

- Paying Bills: Use UPI to pay your electricity, mobile, and DTH bills without any hassle .

The Future of Payments: UPI and IMPS Together

It's important to see these two systems not as competitors, but as teammates. UPI is built on the backbone of IMPS . Every UPI transaction technically runs through the IMPS infrastructure.

What we are witnessing is more a product-portfolio evolution, where UPI has absorbed many of IMPS’s original use cases, while IMPS remains relevant for niche, legacy, and fallback scenarios .

This means UPI is perfect for the front end: the easy, everyday payments. IMPS is the powerful engine in the back that handles the bigger, heavier transfers. Both will continue to play a vital role in India's digital growth.

Quick Decision Guide

Choose IMPS if you are:

- Transferring money above â‚ą1 lakh.

- Want to use a direct bank channel without a third-party app.

- Don't have a smartphone or internet access.

- Paying for business or structured, high-value needs.

Choose UPI if you are:

- Making small, frequent transfers under â‚ą1 lakh.

- Want the quickest, easiest transaction method.

- Paying at a local shop, restaurant, or to a friend.

- Looking for a free and convenient digital payment method.

Frequently Asked Questions

1. Is UPI better than IMPS?

It depends on your need. UPI is better for convenience, speed, and small daily payments as it is free and easy. IMPS is better for large payments over â‚ą1 lakh. There is no one "better" system; there is a right tool for the right job.

2. Which is faster, UPI or IMPS?

Both are real-time systems and transfer money instantly. However, UPI feels faster because it requires fewer steps and has no need for beneficiary registration.

3. What are the disadvantages of IMPS?

The main disadvantages of IMPS include the need to know the receiver's bank account number and IFSC code. You also have to add a beneficiary and wait for activation, and banks usually charge a small fee for the service.

4. Is IMPS safer than UPI?

Both are safe and secure. IMPS uses bank-level verification, while UPI uses two-factor authentication (device + PIN). Neither is "unsafe," but IMPS is often preferred for larger sums due to its direct banking channel.

5. Can I use UPI without an internet connection?

No, not really. UPI works through mobile apps on smartphones, which need an internet connection. A few banks support USSD (*99#) for UPI on basic phones, but it is not as common.

6. What happens if my UPI transaction fails?

If money is debited but the transfer fails, it is usually automatically refunded to your bank account within 3 to 5 business days. The process is automated and you generally don't need to do anything .