Think about the last time you walked into a car dealership. You wouldn't ask the guy trying to hit his monthly sales quota for unbiased driving lessons, right? He knows how the engine works, sure, but his job ends the moment you drive off the lot.

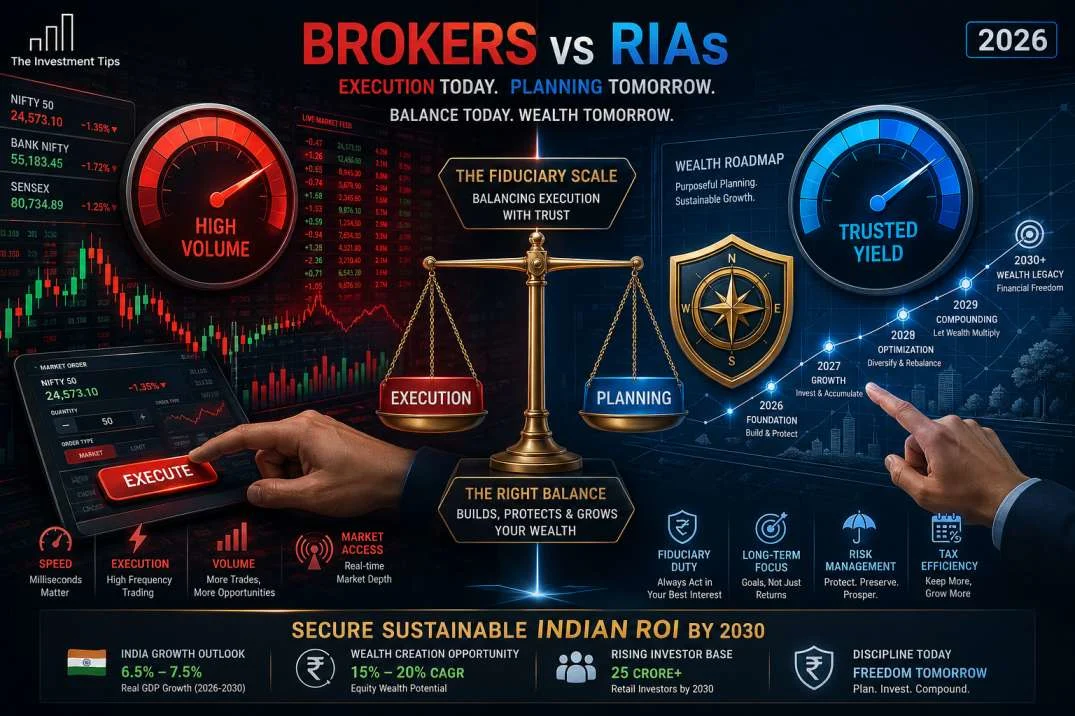

Treating your stock broker like a financial counselor is the exact same mistake. In the 2026 market, the gap between SEBI Registered Investment Advisers vs Stock Brokers India isn't just some boring regulatory "technicality"—it’s the difference between actually growing your net worth and just setting your capital on fire through endless, unnecessary trades. If you aren't sure who you're paying, you're likely the one being played.

The Real Deal: RIA vs. Broker at a Glance

- Who do they work for? RIAs are legally your "fiduciaries" (posh word for: they must put you first). Brokers? They are facilitators. They make the plumbing work.

- How do they get paid? You pay an RIA a clear fee for their brain. Brokers usually eat through your "churn"—earning every time you click 'buy' or 'sell.'

- The "Trust" Check: Never take a "hot tip" without checking the official SEBI registered investment advisor list. If they aren't on it, they’re just a stranger with an opinion.

The Conflict: Execution vs. Advice

The primary difference lies in the "Standard of Care." A stock broker is a transaction agent. Their systems are built for speed, margin funding, and order matching. An Investment Adviser is a fiduciary—a legal term meaning they must put your wallet ahead of theirs.

You may also read :- HDFC Securities Charges Explained: Brokerage, AMC and Hidden Fees

Direct Comparison: RIA vs. Stock Broker

|

Feature |

SEBI Registered Investment Adviser (RIA) |

Stock Broker (Trading Member) |

|

Primary Goal |

Holistic wealth growth & financial planning. |

Efficient execution of buy/sell orders. |

|

Legal Standard |

Fiduciary Duty: Must act in your best interest. |

Suitability Standard: Must suggest "okay" products. |

|

Earnings Model |

Directly from the client (Flat fee or % of AUA). |

Commission-based (Brokerage per trade). |

|

Conflict of Interest |

Low (No commissions allowed from products). |

High (Earns more if you trade more frequently). |

|

Products |

Direct Plans (Mutual Funds), Bonds, REITs, etc. |

Regular Plans, Equities, F&O, Commodities. |

Pro-Tip: Verify, Don't Trust. Always check the SEBI registered investment advisor list on the official SEBI portal. If their name isn't there, they aren't an advisor; they're an unregistered "expert"—and your capital is the guinea pig.

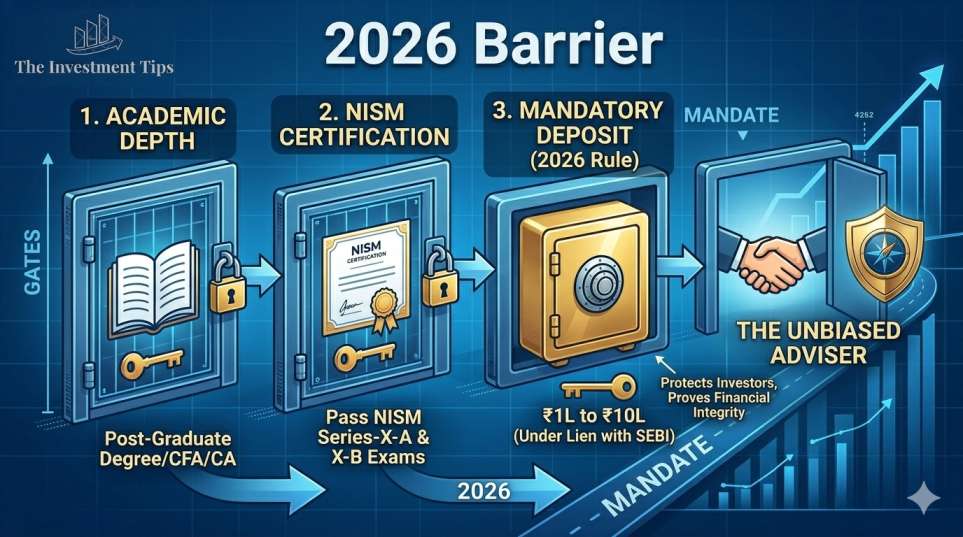

The Professional Barrier: SEBI Registered Investment Advisor Eligibility

In 2026, becoming an RIA is not a weekend hobby. SEBI has made the SEBI registered investment advisor eligibility significantly more rigorous to weed out "fin-fluencers."

- Academic Depth: Must hold a post-graduate degree in finance, accountancy, economics, or a professional qualification like CFA/CA.

- NISM Certification: Must pass NISM-Series-X-A and X-B (Investment Adviser) exams.

- The 2026 "Skin in the Game" Rule: SEBI replaced simple "Net Worth" requirements with a Mandatory Deposit system. Individual RIAs must maintain a deposit (under lien) of â‚ą1 Lakh to â‚ą10 Lakhs depending on the number of clients they serve.

The Hot Take: "Experience" is No Longer Enough

Many veteran brokers claim to be advisors because they've "seen 20 years of markets." In 2026, SEBI doesn't care. If they don't have the NISM certifications and the registered license, their advice is technically illegal. Never pay for "informal" advice from a broker.

Deciphering the Cost: SEBI Registered Investment Advisor Fees

One of the biggest hurdles for retail investors is the "sticker shock" of paying for advice. We are conditioned to think "free" advice from a broker is better. But "free" is often the most expensive price you will ever pay.

The Fee-Only Cap (2026 Rules)

SEBI has standardized SEBI registered investment advisor fees to ensure fairness:

- Flat Fee Model: Capped at â‚ą1.51 Lakh per annum per family.

- Asset Under Advice (AUA) Model: Capped at 2.5% of the assets they are advising on.

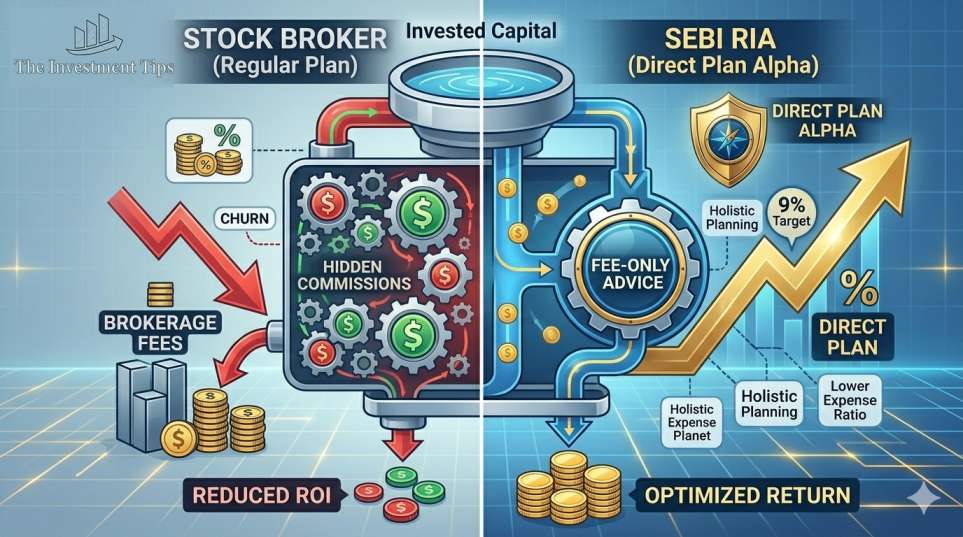

Technical "Under-the-Hood": The Direct Plan Alpha

When an RIA suggests a Direct Plan of a Mutual Fund, the expense ratio is usually 0.75% to 1% lower than the "Regular Plan" your broker offers. On a â‚ą50 Lakh portfolio, that’s â‚ą50,000 saved every year in hidden commissions. This saving often pays for the RIA's fee entirely.

Finding the Elite: The Top 10 Investment Advisors in India

Finding the right advisor is like dating; you need to find a match for your risk appetite. While we can't name one "best" advisor for everyone, the top 10 investment advisors in India are typically defined by their transparency and fee-only status.

A Real-World Scenario: The "Churn" Trap

Consider an investor, Rahul. His broker suggested he "rebalance" his portfolio four times a year. Each move cost brokerage, STT, and capital gains tax. The broker earned â‚ą40,000 in commissions.

Rahul then hired an RIA who changed the strategy to "Buy and Hold" using index funds. Rahul paid the RIA a â‚ą25,000 fee but saved â‚ą60,000 in taxes and brokerage. His net ROI increased simply by doing less.

FAQ: Punchy Answers for the Strategic Investor

Q: Can a broker provide advisory services?

A: Only through a separately identifiable department or subsidiary that is registered as an RIA. They must keep "Execution" and "Advice" at arm's length to prevent misselling.

Q: Where can I see the SEBI registered investment advisor list?

A: It is publicly available on the SEBI website (sebi.gov.in) under the "Intermediaries" tab.

Q: Why are RIAs moving to a "Deposit" model in 2026?

A: To ensure they have liquid assets to pay for any regulatory penalties or client compensations, increasing the trust factor for retail investors.

Q: Are there any exempted professionals?

A: CAs and Lawyers can give incidental advice (e.g., a CA suggesting an ELSS for tax saving), but they cannot charge a separate "Advisory Fee" without being an RIA.

Final Verdict: The 2026 Wealth Strategy

The battle of SEBI Registered Investment Advisers vs Stock Brokers India is a battle for your financial sovereignty. Use a broker for what they are good at: high-speed execution and technology. Hire an RIA for what you need: a roadmap that isn't biased by commissions.

Pay for the architect, use the best tools for the construction. It works. Until you ignore the regulation—then it doesn't. Stay sharp.